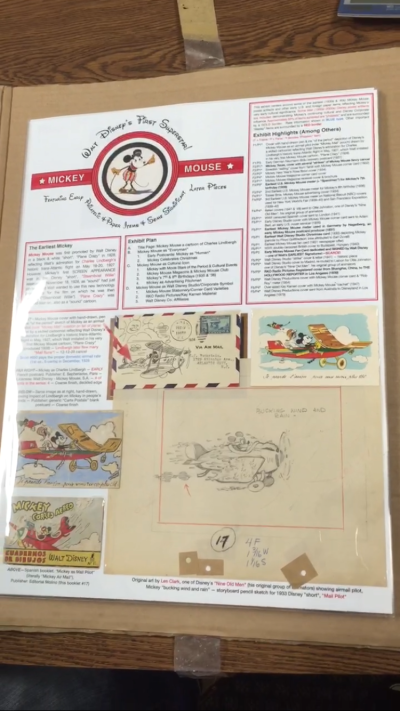

Edward Bergen has been an avid philately of Disney memorabilia for over 30 years. One of his collections is a compilation of stamp and postal memorabilia in honor of the Disney Icon Mickey Mouse titled, Walt Disney’s First Superstar: Mickey Mouse. This collection is valued between $30-35,000 . Another collection of his is titled Walt Disney Postal Commemoration of 1968 is valued around $25-30,000.

These collections will also be presented at the International Stamp Show at the Javitz center in New York from May 28th to June 4th 2016. A book based on his collections will published on Amazon titled identically to Bergen’s exhibit, Walt Disney’s First Superstar: Mickey Mouse. This book includes 3 volumes with 52 pages in each of them. Here is the link to the pictorial book. The proceeds from these volumes will benefit the Carl Barks Fan Club.

Carl Barks is the creator/designer of the immortal Mickey Mouse, as well as his companions : Donald Duck, Minnie Mouse, and Goofy. His career spanned over 60 years as a cartoonist starting in 1935 in the Disney Animation department. He single-handedly wrote and drew nearly 500 “Duck Stories” for the Disney Comic Books: Walt Disney’s Comics & Stories, The Donald Duck Adventures, and The Uncle Scrooge Adventures.

These greeting cards, stamps, and editorial pictures are not just simply Disney themed artwork. These are pieces of history which also tell a narrative about the customs of American society from the 1920’s to the 60’s. These pictorials within Walt Disney’s First Superstar: Mickey Mouse, chronicle the evolution of Mickey Mouse as the decades pass by. These valuable pieces of history are kept in a fireproof alarmed safe while at home, but requires additional coverage while it is on display. Always make sure to talk with your agent before displaying your collections to ensure proper coverage.